Tax Code

Tax Code and SST-02 Mapping

The images below show SST tax code structures and mapping to SST-02:

Part A:

Part B1:

Part B2:

Part C:

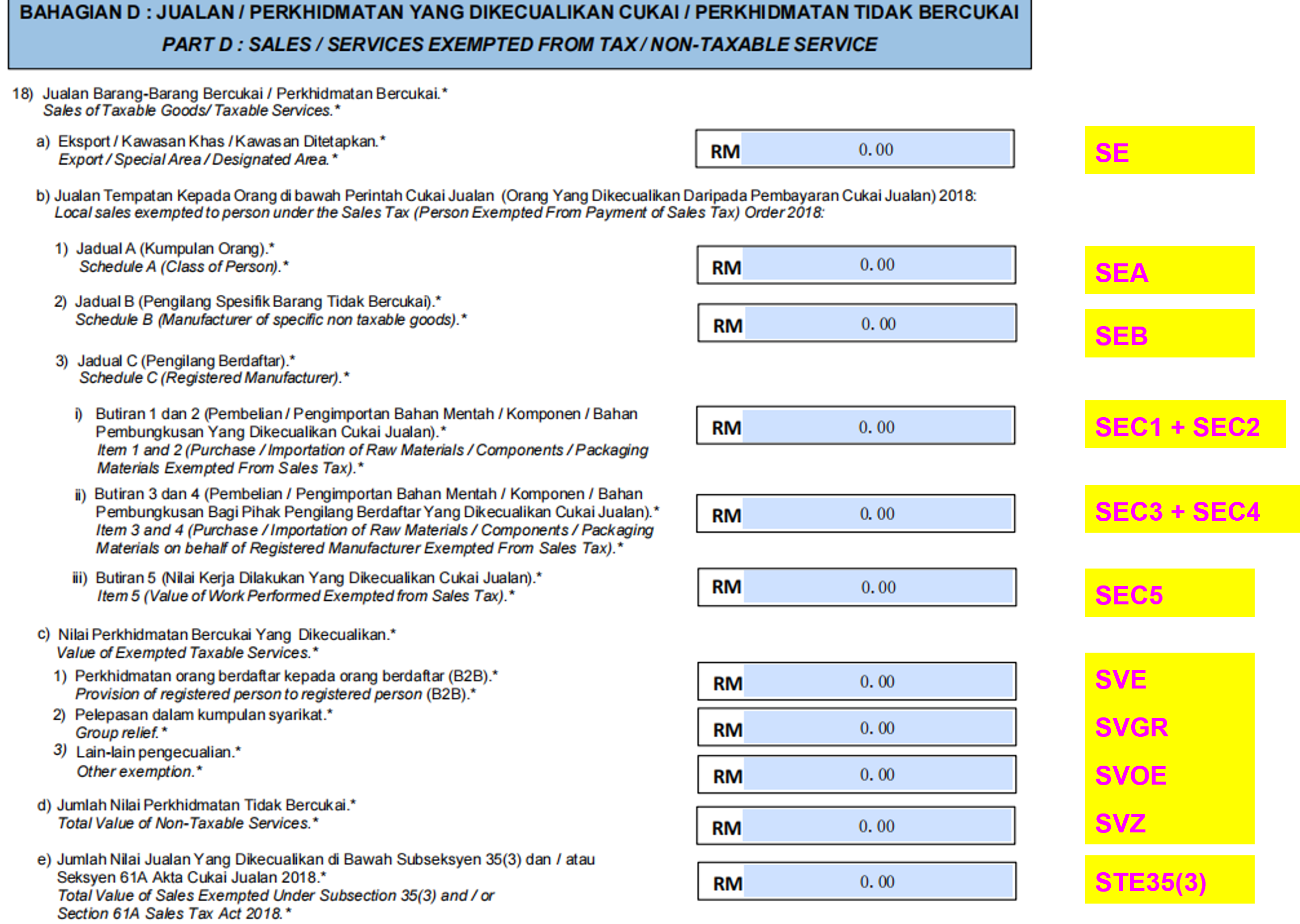

Part D:

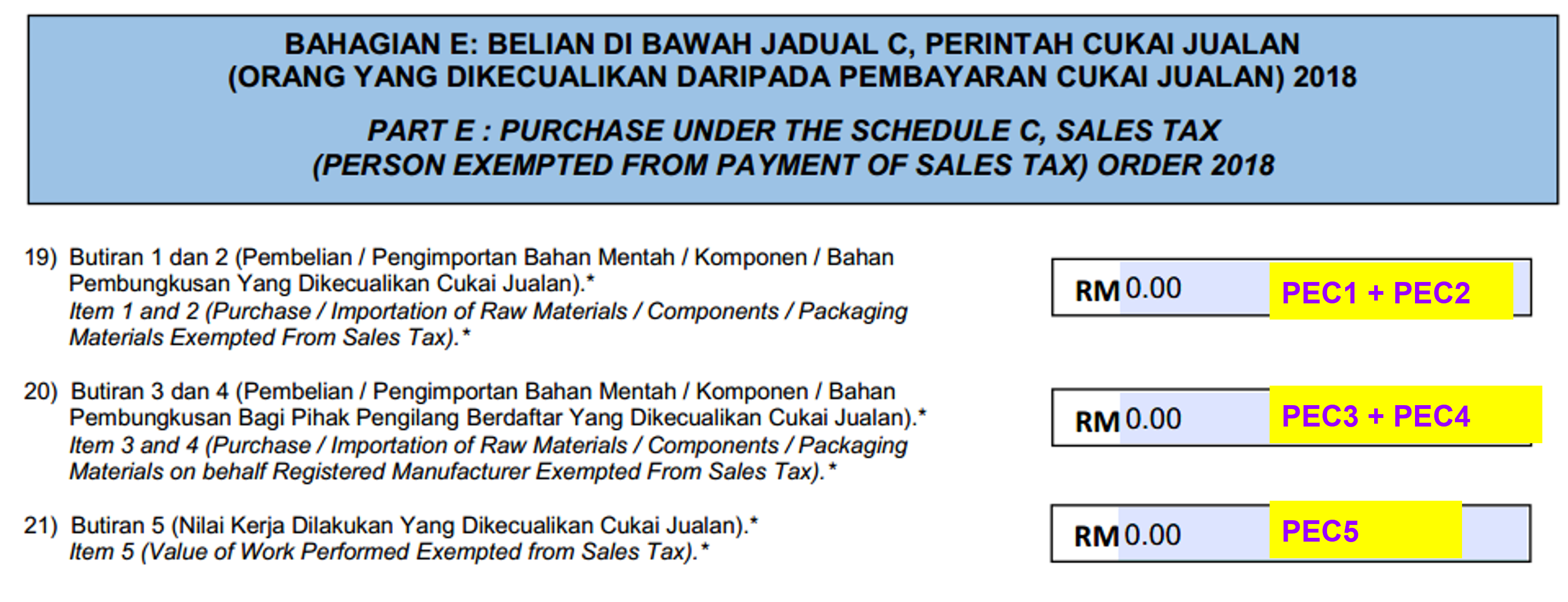

Part E:

Part F:

Part G:

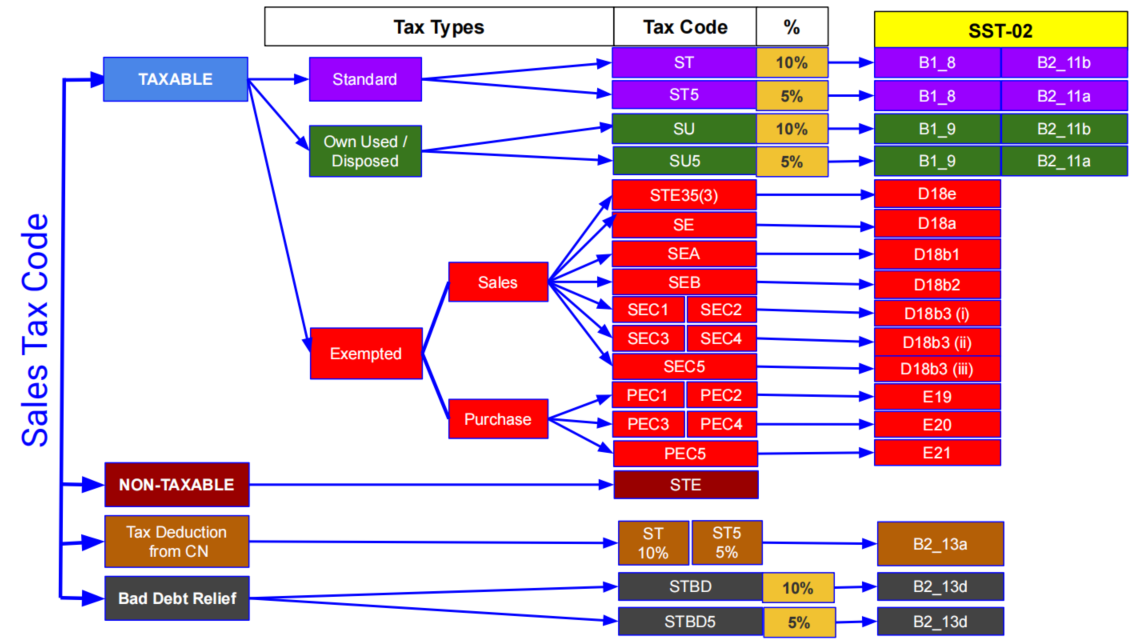

Sales Tax Code

-

Standard

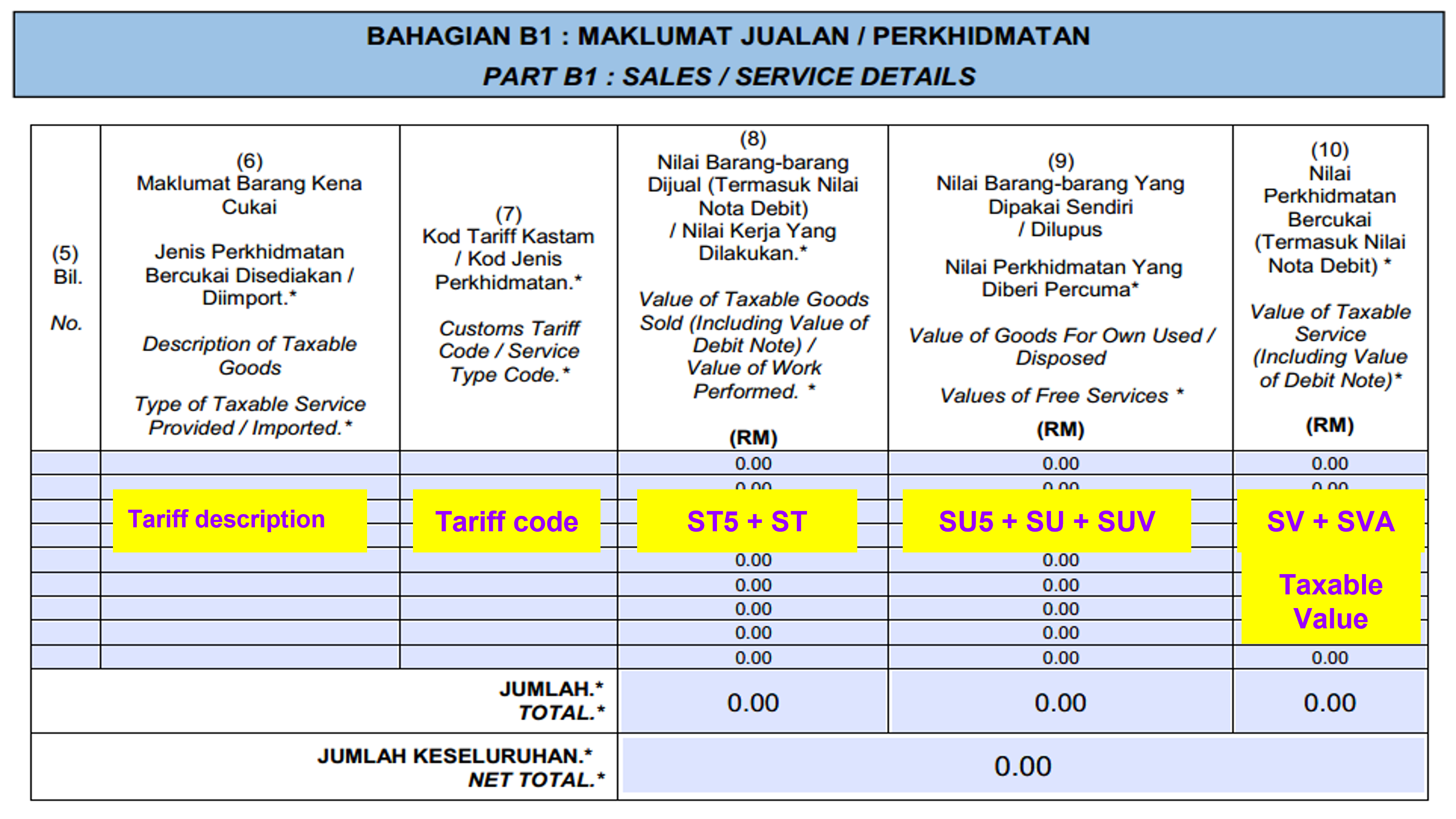

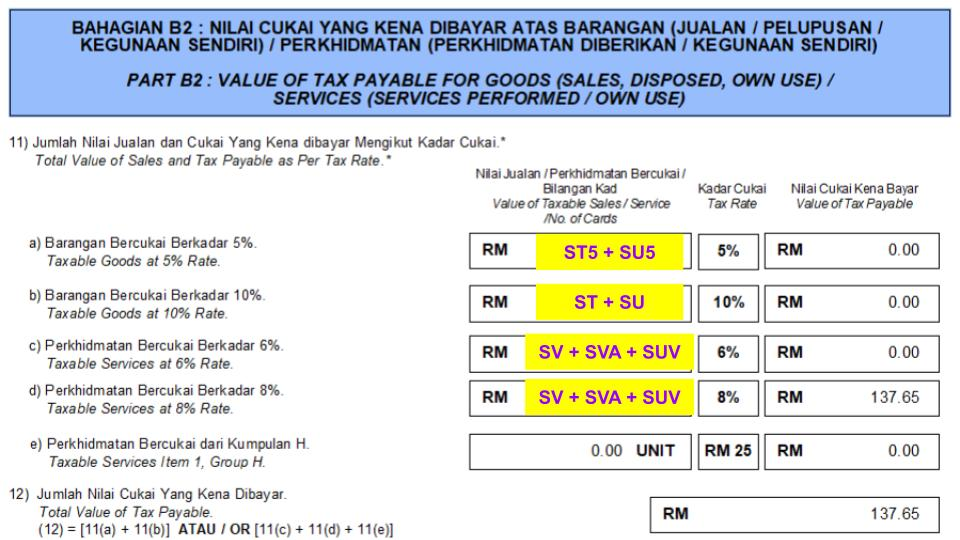

No Tax Code Description Application Tax Rate SST-02 01 ST Sales Tax 10% charged to the taxable goods based on accrual/billing basis Manufacture/processed products sold to local company at tax rate 10% 10% B1_8, B2_11B 02 ST5 Sales Tax 5% charged to the taxable goods based on accrual/billing basis Manufacture/processed products sold to local company at tax rate 5% 5% B1_8, B2_11A -

Deemed Supply (Own Used/Disposed)

No Tax Code Description Application Tax Rate SST-02 01 SU Goods Own Used/Disposed deemed taxable and charged at 10% based on accrual/billing basis Products produced and self use it are deemed taxable at tax rate 10% 10% B1_9, B2_11B 02 SU5 Goods Own Used/Disposed deemed taxable and charged at 5% based on accrual/billing basis Products produced and self use it are deemed taxable at tax rate 5% 5% B1_9, B2_11A -

Sales - Exempted

No Tax Code Description Application Tax Rate SST-02 01 STE Sales Tax Exempted on goods as prescribed in the Sales Tax (Goods Exempted From Tax) Order 2018 Specific manufacture products which are exempted from tax, eg. rice flour Exempted 02 SE Sales Tax Exempted to Export, Special Area (SA) Manufacture/processed products export to oversea or special area at tax rate exempted, eg. Free Zone, LMW and Area (DA), eg. Langkawi, Tioman, Labuan Exempted D18_A 03 SEA Sales Tax Exempted-Sch A Class of Person, eg. Government, Local Authority Dept, etc. Detail refer to Schedule A in Sales Tax (Person Exempted From Payment Of Tax) Order 2018 Exempted D18_B1 04 SEB Sales Tax Exempted-Sch B Manufacturer of specific non-taxable goods. e.g. control products, medical. Detail refer to Schedule B in Sales Tax (Person Exempted From Payment Of Tax) Order 2018 Exempted D18_B2 05 SEC1 Sales Tax Exempted-Sch C (Item 1) Raw materials, components and packaging materials excluding PETROLEUM imported/purchased from a reg. manufacturer/licensed warehouse by any reg. manufacturer Exempted D18_B3 (i) 06 SEC2 Sales Tax Exempted-Sch C (Item 2) Raw materials, components and packaging materials imported/purchased from a reg. manufacturer/licensed warehouse by any reg. manufacturer of PETROLEUM products Exempted D18_B3 (i) 07 SEC3 Sales Tax Exempted-Sch C (Item 3) Raw materials, components and packaging materials excluding PETROLEUM imported/purchased from a reg. manufacturer by any agent on behalf of a reg. manufacturer Exempted D18_B3 (ii) 08 SEC4 Sales Tax Exempted-Sch C (Item 4) Raw materials, components and packaging materials imported/purchased from a reg. manufacturer by any agent on behalf of a reg. manufacturer of PETROLEUM products Exempted D18_B3 (ii) 09 SEC5 Sales Tax Exempted-Sch C (Item 5) Semi-finished taxable goods or finished taxable goods which are subsequently returned by a subcontractor to a reg. manufacturer after completion of subcontract work Exempted D18_B3 (iii) 10 STE35(3) Total value of Sales Exempted Under Subsection 35(3) and / or Section 61A Sales Tax Act 2018 Products produced can be exempted and approved by Minister under Subsection 35(s) and / or Section 61A Sales Tax Act 2016 Exempted D18E -

Bad Debt Relief

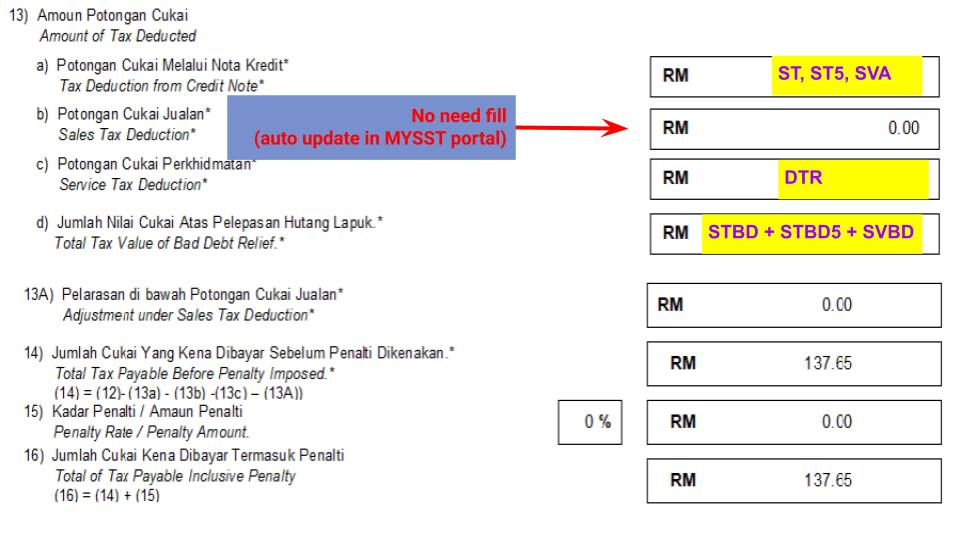

No Tax Code Description Application Tax Rate SST-02 01 STBD Sales Tax Bad Debt Relief at tax rate 10%. Claimable within 6 years from the taxable service date, subject to DG approval A registered sales tax company can request a tax refund for the paid sales tax from customs if unable to recover the arrears from the customer. 10% B2_13d 02 STBD5 Sales Tax Bad Debt Relief at tax rate 5%. Claimable within 6 years from the taxable service date, subject to DG approval A registered sales tax company can request a tax refund for the paid sales tax from customs if unable to recover the arrears from the customer. 5% B2_13d

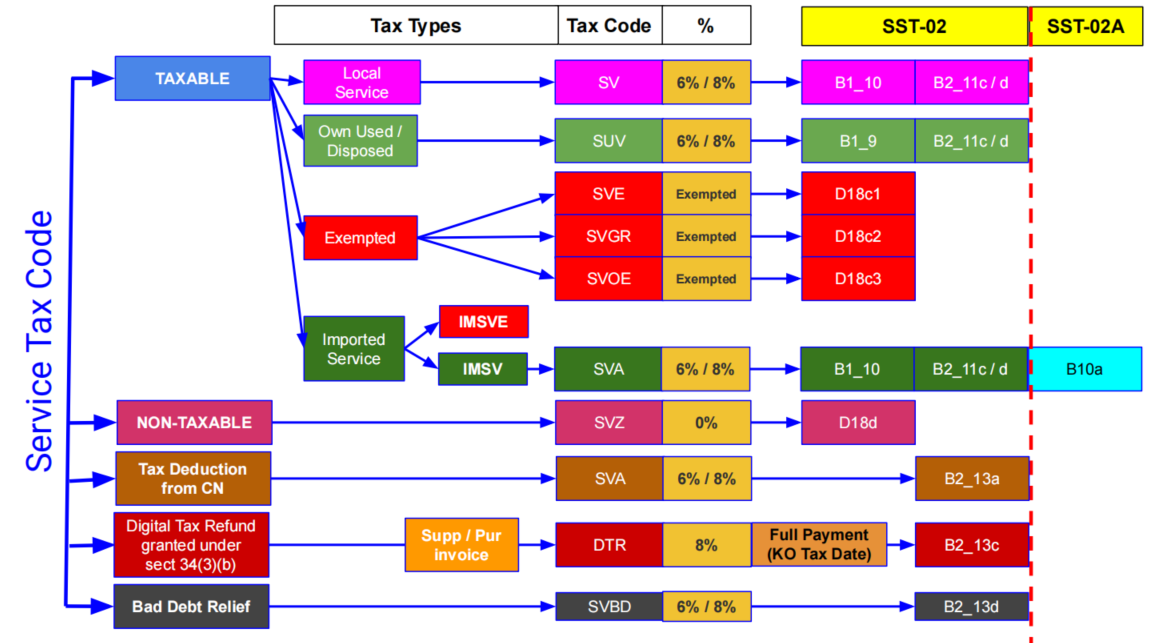

Service Tax Code

-

Standard

No Tax Code Description Application Tax Rate SST-02 01 SV Service Tax 6% / 8% charged to the taxable services based on payment basis Service transaction charged at 6% / 8% follow the nature of business. Accounting as payment basis 6% / 8% B1_10, B2_11C/D 02 SVA Service Tax 6% / 8% charged to the taxable service based on accrual/billing basis. It is used in IMSV tax code to report in SST-02A Service transaction charged at 6% / 8% follow the nature of business. Accounting as Accrual/Billing basis 6% / 8% B1_10, B2_11C/D -

Deemed Supply (Own Used/Disposed)

No Tax Code Description Tax Rate SST-02 01 SUV Service Own Used charged at 6% / 8% on accrual/billing basis 6% / 8% B1_9, B2_11C/D -

Service Exempted

Applicable to same service provider under:

- Group G to Group G (all except Employment and Guards protection service provider).

- Group I to Group I (ie. advertising service provider).

No Tax Code Description Application Tax Rate SST-02 01 SVE Service Tax Exempted between same service providers in Group G (excluding item j and k) or in Group I item 8 only. Refer to Service Tax (Person Exempted From Payment of Tax) Order 2018 B2B Exemption Exempted D18C1 02 SVGR Service Tax Exempted related to Intra Group Relief Group Relief Exempted D18C2 03 SVOE Service Tax Exempted - Others Other exemptions besides B2B exemption and Group Relief (eg. Non-reviewable contracts are granted exempted for 1 year) Exempted D18C3 -

Imported Service

- For non-Service Tax Registered must declare using SST-02A.

- For Service Tax Registered must declare using SS-02.

No Tax Code Description Input Tax Output Tax SST-02 SST-02A (for imported service) 01 IMSV Imported Service Tax, any company in Malaysia who acquire the taxable service from company outside Malaysia. Non-SST & Sales Tax reg. must report in SST-02A. Service tax reg. remains report in SST-02 PSV (8%) SVA (8%) B1_10 B2_11C B10a 02 IMSVE Imported Service Tax Exempted between same service providers in Group G (excluding item j and k) or in Group I item 8 only. Refer to Service Tax (Person Exempted From Payment of Tax) Order 2018 PSVE SVE D18C -

Non-Taxable

No Tax Code Description Application Tax Rate SST-02 01 SVZ Non-taxable services refer to transactions not subject to service tax eg. healthcare facility given to citizen, residential buildings, related public amenities, etc Not Subject to Service Tax D18D -

Bad Debt Relief

No Tax Code Description Application Tax Rate SST-02 01 SVBD Service Tax Bad Debt Relief at tax rate 6%. Claimable within 6 years from the taxable service date, subject to DG approval A registered service tax company can request a tax refund for the paid service tax from customs if unable to recover the arrears from the customer. 6% / 8% B2_13D

Purchase Tax Code

-

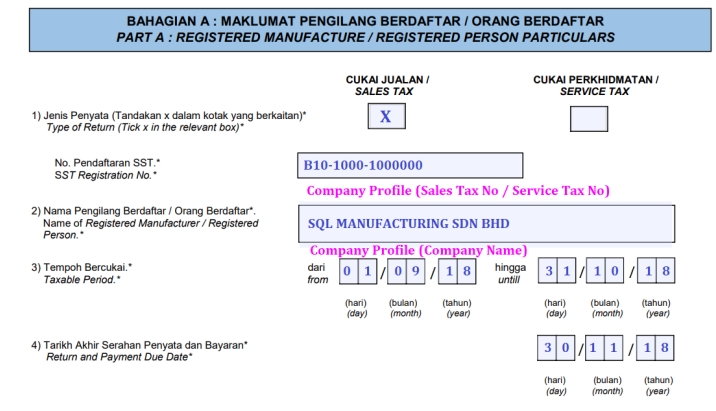

Need Declare In SST-02

No Tax Code Description Application Tax Rate SST-02 01 PEC1 Purchase Tax Exempted-Sch C (Item 1) Raw materials, components and packaging materials excluding PETROLEUM imported/purchased from a reg. manufacturer/licensed warehouse by any reg. manufacturer Exempted E19 02 PEC2 Purchase Tax Exempted-Sch C (Item 2) Raw materials, components and packaging materials imported/purchased from a reg. manufacturer/licensed warehouse by any reg. manufacturer of PETROLEUM products Exempted E19 03 PEC3 Purchase Tax Exempted-Sch C (Item 3) Raw materials, components and packaging materials excluding PETROLEUM imported/purchased from a reg. manufacturer by any agent on behalf of a reg. manufacturer Exempted E20 04 PEC4 Purchase Tax Exempted-Sch C (Item 4) Raw materials, components and packaging materials imported/purchased from a reg. manufacturer by any agent on behalf of a reg. manufacturer of PETROLEUM products Exempted E20 05 PEC5 Purchase Tax Exempted-Sch C (Item 5) Semi-finished taxable goods or finished taxable goods which are subsequently returned by a subcontractor to a reg. manufacturer after completion of subcontract work Exempted E21 06 DTR Digital Tax refund granted under section 34(3)(b) Service Tax Act 2018 by the offetting method based on the actual amount paid Local service registered person who has paid imported digital service tax to a Foreign Service Provider (FSP). It is allow to claim a refund granted under section 34(3)(b) Service Tax Act 2018. 8% B2_13C -

No Need Declare In SST-02

No Tax Code Description Application Tax Rate SST-02 01 PST Purchase Sales Tax 10% Apply for purchase transactions involve Sales Tax rate at 10%. No claimable from Kastam. 10% 02 PST5 Purchase Sales Tax 5% Apply for purchase transactions involve Sales Tax rate at 5%. No claimable from Kastam. 5% 03 PSV Purchase Service Tax 6%,8% Apply for service transactions involve Service Tax rate at 6% / 8%. No claimable from Kastam. 6% / 8% 04 PSVE Purchase Service Tax Exempted Apply for service transactions which is under same service providers between Group G (excluding item j and k) or Group I (item 8 only) or in Group J. Exempted

Tariff Code

- Tariff classification is a complex yet extremely important aspect of cross-border trading.

- Goods imported from or to Malaysia are classified by the Harmonized Tariff Schedule (HTS) or commonly referred to as HS Codes.

- The codes, created by World Customs Organization (WCO), categorize up to 5,000 commodity

- HS Codes are made of 6-digit numbers that are recognized internationally, though different countries can extend the numbers by two or four digits to define commodities at a more detailed level.

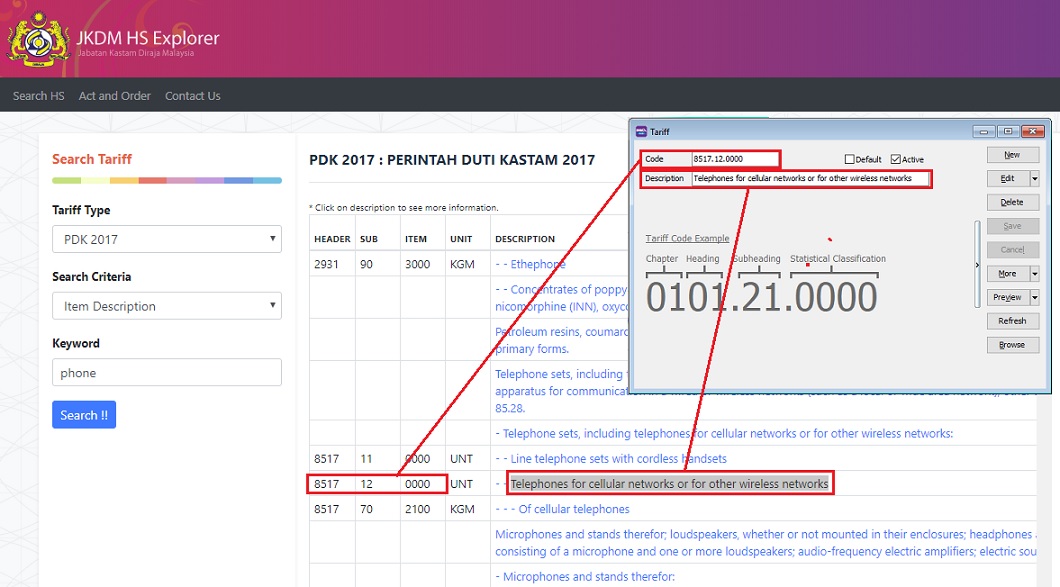

- Click this link here to search the tariff code list from Kastam system.

Quick Setup for Tariff Code

-

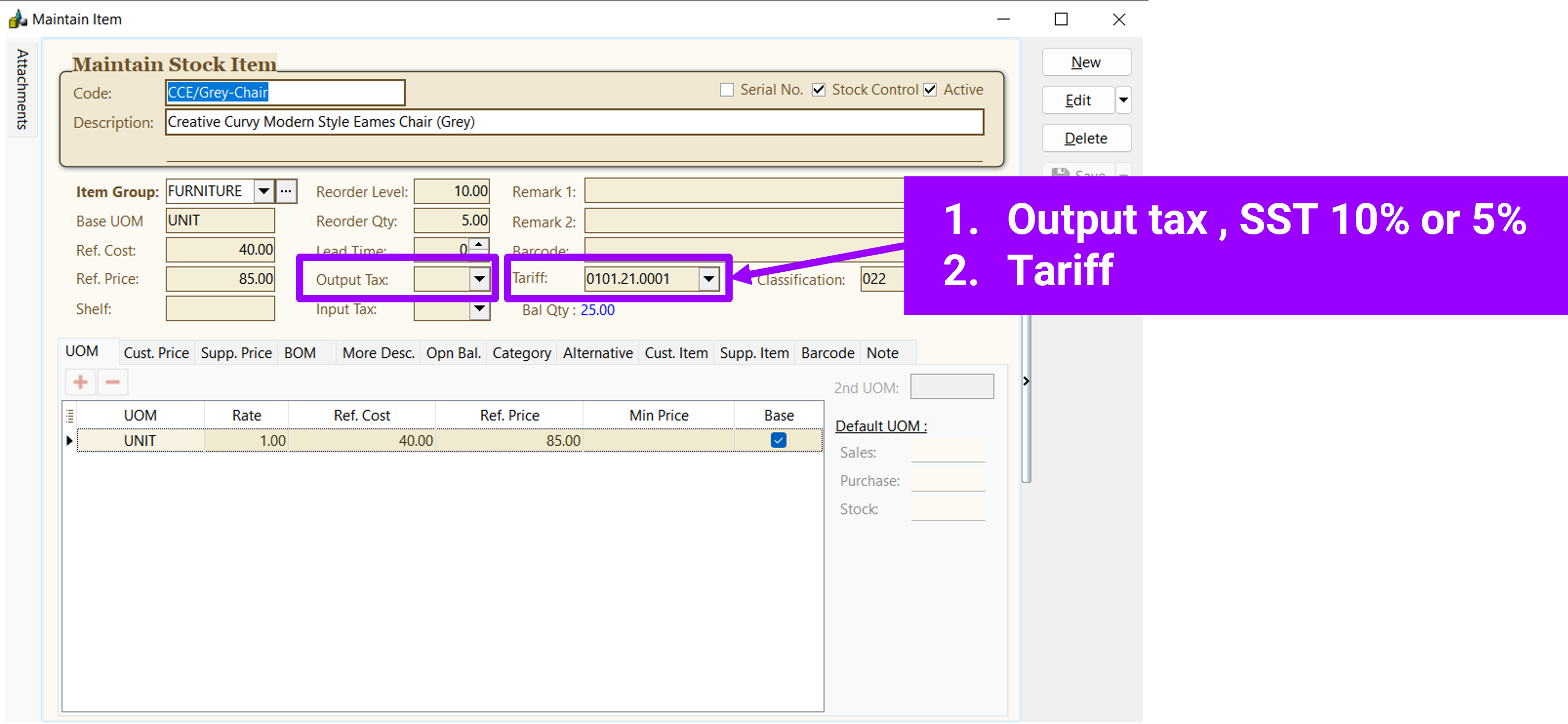

Create the tariff code applicable to your product at Maintain Tariff.

-

Pick a tariff code for an items at Maintain Stock Item.

-

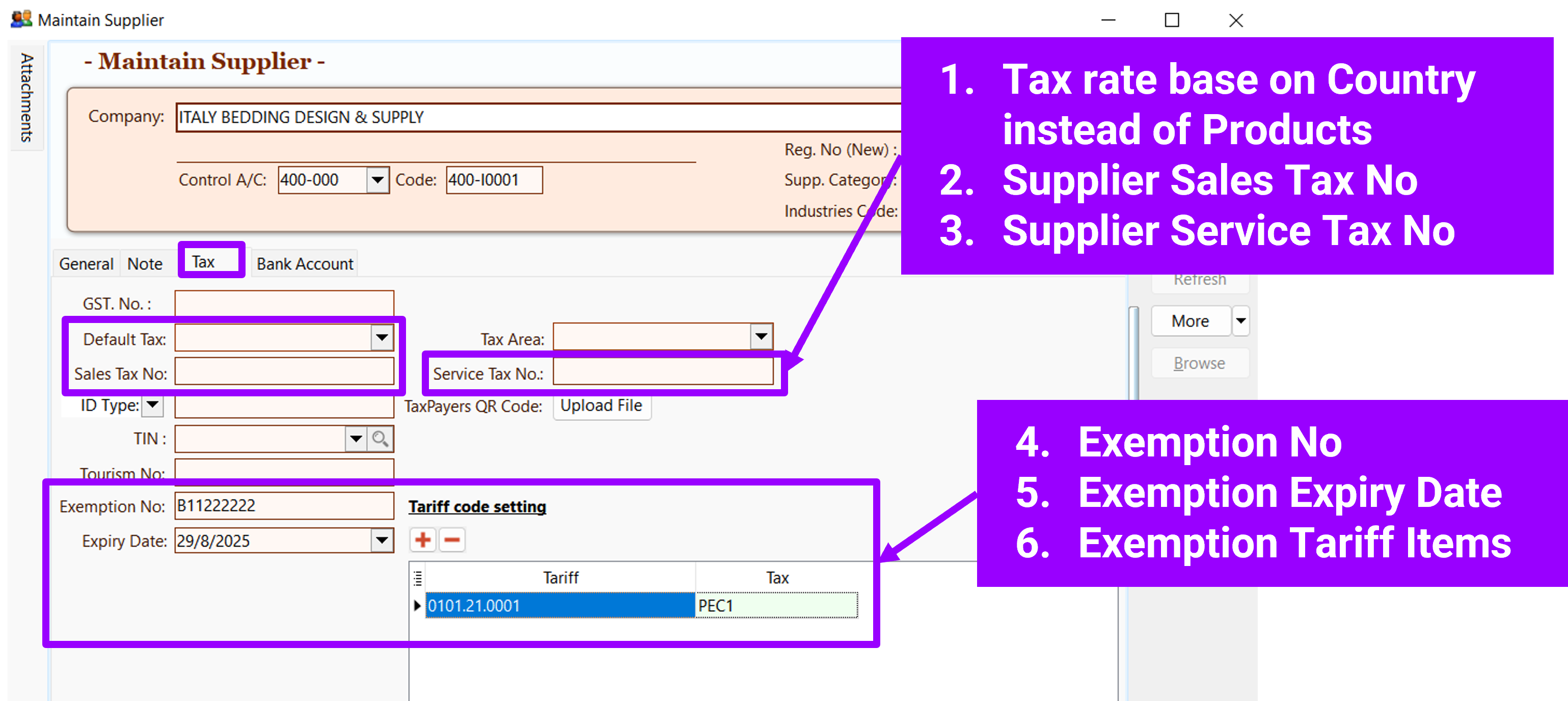

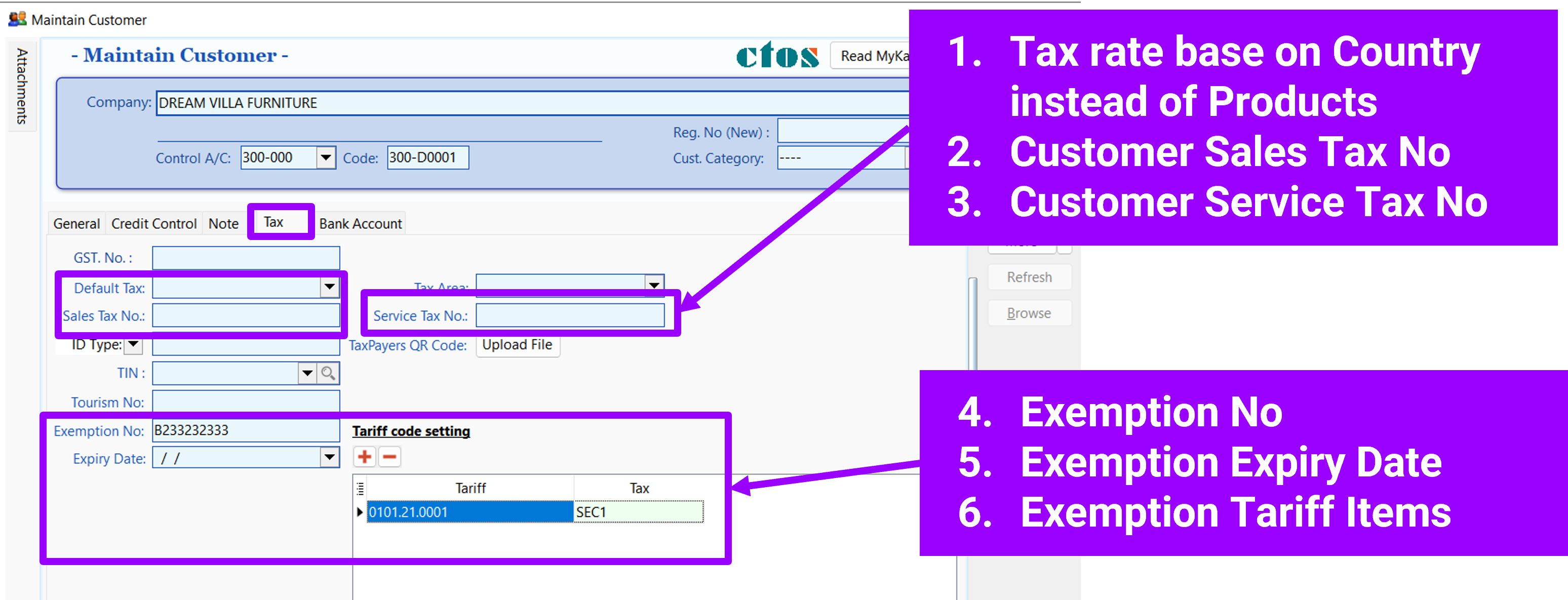

For exemption certificate case (under Schedule A, B, C), a tariff and tax code (SEA, SEB, SEC1, SEC2, SEC3, SEC4, SEC5) should set in Maintain Customer and Maintain Supplier (Tariff code setting under Tax Tab).

Maintain Customer

Maintain Supplier